Over the past few months, the acceleration of Yen’s weakening vs the US dollar has pushed several economists and investors to claim Japan was engaged in a currency crisis.

As a reminder, a currency crisis occurs when a country’s currency exchange rate vs all other major currencies declines rapidly and out of any control. It is most often triggered by investors and traders’ conviction that the currency’s exchange value should be lower than it is owing to financial and economic fundamentals that have changed – and worsened.

Discussing the possibility of a currency crisis concerning the Yen will give me the opportunity to explore Japan’s economic fundamentals and its financial and monetary experiment that has begun thirty years ago and inspired other Central Banks. I will also anticipate the domestic and international consequences of a Yen’s strengthening or continuous depreciation against the US dollar.

The USD-JPY exchange rate evolution

As shown in the below graph, since Q1 2022 the USD-JPY exchange rate has experienced an upward trend. From 115.6 in 03/01/2022, it has jumped to 148.7 in 10/09/2022. The Bank of Japan subsequently interfered in the FX market, buying up to Y9.19trn between September 22th and October 24th to prop up the value of its currency. It has proven to be insufficient, since the USD-JPY after a short decrease has pursued its rise to break the symbolic barrier of 150 in 3Q23 (151.1 as of November 6th 2023). It has been consistenly above this level since April 2024.

As of May 10th, the USD-JPY X-rate’s 52week range was 135.6 – 160, far above its range between 2004 and 2021. As seen below, over the past two decades the USD-JPY X-rate stood between 100 and 120 except between 3Q08 and 2Q13, notably due to the 2008 Great financial crisis which had hit for a time the trust in the US dollar.

A USD/JPY exchange rate above 150 hadn’t been seen since 1990, 34 years ago. In the aftermath of the Bretton Woods monetary system’s, where the USD/JPY X-rate was fixed at 360, the Japanese government has manipulated the FX market for maintaining a weak yen against the dollar to support its export-led growth model. However the Yen has appreciated by step over the next two decades following 1971, notably after the 1985 Plaza Agreements.

The yen depreciation against the dollar over the past two years coupled with the BoJ’s ineffective FX interventions, in October 2022 and May 2024 are encouraging some analysts to speak about a currency crisis.

Why would the Yen depreciate out of control ?

In theory, moves in an exchange rate can be explained by the evolving interest rate differential between the two countries’ currencies. In this regard, the Yen’s 10% depreciation YTD vs the US dollar makes sense, as the Fed and BoJ’s monetary policies have been at odds over the past 2 years. Since 2022, the Fed has engaged in an agressive monetary tightening, increasing the federal funds rate target range from 0.00-025% in 1Q22 to 5.25-5.50% in 3Q23, a range which has remained unchanged ever since.

Meanwhile, the Bank of Japan has until very recently stuck to the three pillars of its ultra-loose monetary policy.

-a negative call rate target range , at -0,1% the call rate being the equivalent of the federal funds rate ( the overnight uncollateralized borrowing rate between commercial banks ).

-the Quantitative and Qualitative Easing (QEE) monetary policy which was enforced in 2013 but already used between 2001 and 2006.

-the Yield Curve Control, a new form of QEE introduced in 2016 which aims at buying 10-Y Japanese government bonds to keep their YTM below 1%. The Bank of Japan had the intention to control not only short-term interest but also long-term interest rates through the control of Long-term government bonds’ yields.

All these measures have resulted in a much higher rentability of US fixed-income assets compared to Yen-denominated fixed-income assets, encouraging Japanese investors to convert Yen to US dollars and buy US fixed-income assets.

However, this analysis may limit the scale of the Yen depreciation since it could be solved by the reduction in interest rates differential. As an example, in January 2016, the Fed had started hiking rates while at the same time the BoJ’s call rate remained negative. At that time, the interest rate differential between the two countries increased, which in our logic would have pushed the Yen down. Yet, the USD-JPY exchange yet weakened, i.e the Yen strengthened. Yen recent evolution may be thus not only linked with the issue of interest rates.

The current depreciation of the Yen may underline the fact investors realize that the Yen is structurally cheaper than its current level due to Japan’s deteriorating financial and economic fundamentals.

Early in the year indeed The Bank of Japan had appeared to be trapped by its past choices. Since mix of unconventional policies it implemented starting 2001 to cope with structural deflation weren’t successful, since In 1998 as well as in 2020, Year-on-year inflation rate stood around 0%. But the combination of QEE and YCC has resulted in the the Bof’s balance sheet more than tripling its size between 2012 and 2024 while at the same time its FX reserves have barely evolved. Japan’s FX reserves amount to $1.223 trn, which is the equivalent in US dollar of Japan money supply expansion (M2 aggregate) between 2020 and 2024. Most of this money printed out of nowhere has financed the expansion of Japan’s public debt, whose ratio to GDP rose from 186% in 2013 to 261% in 2023.

Japan’s liabilities have increased but at the same time the income it generates to pay back this debt has stagnated. Japan’s real GDP expressed in US dollars actually declined over the past decade and mainly due to a decreasing productivity factor and an absolute decline in the working population, the country’s long-term structural growth is below 0,5%.

As highlighted by many economists and investors such as Ray Dalio, whose essay is summed up here , when a country is far advanced in its long term debt and money cycle, which corresponds to the acceleration of money printing and debt accumulation without an equivalent creation of income to meet this promises of payment, the country’s currency will soon face mistrust from foreign investors, which will either dump their holdings of fixed income assets denominated in this currency or short-sell the currency itself. The latter is currently happening for the Yen, as the Japanese population actually owns over 90% of its country’s public debt. Arguably, Japan’s ownership of its own public debt may be the main reason why the Yen didn’t depreciate earlier.

The Japanese Yen is not weak ; the US dollar is too strong.

One should never neglect the fact an exchange rate is a relationship between two variables. The USD-JPY exchange rate may be durably increasing owing to Japan’s economy doomed to deteriorate in the long-term, but it could be also the result of an abnormal US dollar strength.

Analysing the USD-JPY X-rate require to consider the US’s currency status. I won’t delve into the advantages of this status brings, but one should keep in mind it structurally strengthens the US dollar relative to the US economic fundamentals, notably its current account balance. US has a structural negative current account balance, while Japan had current account balance of 2,1% of its GDP in 2022, fluctuating between 2% and 4% over the past 15 years. Japan had a trade surplus of $71bn with the US as of 2023, which is also structural. Considering the real determinants of an exchange rate, the Japanese yen is arguably under-evaluated.

Considering also the purchasing power parity (PPP) theory which is another real driver of exchange rate change, one could defend an undervaluation of the Yen. Indeed, according to the PPP theory, a currency’s exchange rate is due to the differential the considered country’s inflation rate and foreign countries’ and in the long-term the exchange rate evolves so that the price of a good is the same in the two countries. Japan’s cumulative inflation has been +5,3% between 2020 and 2023, vs 17,73% in the US.

Consequently, according to the OCED, using the PPP method the USD-JPY exchange rate has actually decreased from 116.8 to 94.9 between 2008 and 2022, which means the Yen has appreciated in theory against the US dollar and that it was under-evaluated by around 40% in 2022 (end of year 2022 USD-JPY X-rate was at 132).

Lastly, Japan’s monetary distress has to be compared with the country’s outstanding FX reserves and holdings of FX reserves, coupled with an Japanese companies’ sizeable assets abroad. Japan has compensated the weakness of the Yen by accumulating fixed income foreign assets. the BoJ’s reserves of foreign fixed income assets amounted to 30% of its GDP, versus 20% in 2012. Private institutions and the Government Pension Investment Fund’s holdings of foreign debt have also increased over the past 10 years, which results in Japan’s holdings of fixed income assets representing 80% of its GDP (60% in 2012). As a reminder, the GPIF is the largest pension fund in the world and holds also important amounts of foreign stocks.

Japanese companies’ overall foreign portfolio investments were 628.45 trillion yen ($4.2 trillion) in 2023. They were notably sustained by 20 years of corporate debt reduction and corporate reforms, leading to the accumulation of cash reserves by Japanese companies, which then re-invested them abroad. All in all, a further decrease in the Yen can be still offset because Japanese financial and monetary institutions have financial powder, and because the Japanese population’s decline in purchasing power is offset by its wealth accumulated in currencies with better returns.

What follows ? Scenarios and discussions about the future USD-JPY exchange rate.

Before exploring the scenarios, I would like to point out one hypothesis. Most of the current analysis on Japanese Yen start from the underlying assumption that the USD-JPY strengthening is unwanted. But what if the Bank of Japan, despite its communication has the intention to let the JPY slide against the US dollar? As I will describe later, there is an interest for Japan in letting its currency drop.

The JPY further depreciates

The short and medium-term increase of the USD-JPY rate seems inevitable given the monetary deadlock Japan is facing right now. In march 2024, the Bank of Japan ended its non-conventional policy by increasing the call rate range target between 0 and 0,1% and by signalling the end of the YCC. The Bank officially justified the end of its policy given the return of an inflation rate above 2%, which was its goal, and the development of a “virtuous cycle between inflation and wages”.

However inflation in Japan is not due to BoJ’s policy, but is the consequence of external factors (energy and food prices volatility since 2021 and the Ukraine war) whose cost is actually worsened by the weakening Yen, since Japan imports almost all of its energy and food consumption. At the same time, though Japanese trade unions have secured the biggest wage increase in 30 years in December 2023, in 1Q24 household spending declined, undermining the idea of a inflation-wage increase beneficial for domestic consumption.

In a word, Japan combines a weak domestic demand recovery coupled with a durable debt problem making any substantial rise in government bond yields unsustainable. As a consequence, the markets are anticipating that the BoJ’s timid start of normalisation to be short-lived and the differential of interest rates with the US to remain unchanged, triggering a short-selling of JPY.

The JPY depreciation would increase imported inflation (food and energy mainly) so actually most of the burden would be born by Japanese population. However, it may give Japanese exporting companies a tremendous competitive advantage. This is a direct threat to countries that have already trade deficits with Japan (Anglo-saxon countries) but also with the three countries that directly competes with Japanese exporting champions : Germany, South Korea and China. From this point of view, The Bank of Japan could also accommodate to this trend and even reinforces it.

Unwanted or not, Japan’s depreciating currency will press China and South Korea to depreciate their currencies in order to stay cost competitive, which will leave Germany the most vulnerable of Japan’s competitor, as it has little means to interferes in the forex market to limit EUR/JPY appreciation (also at a record high).

The JPY reverses its trend and appreciates

Real factors that play an important role in a currency’s long-term exchange rate play in favour of a Yen appreciation. As said, Japan’s structurally low inflation owing to its depopulation and its structurally current account surplus indicate in a near to distant future the re-appreciation of the Yen vs the US dollar.

This move would occur as a consequence of the US dollar losing its credibility as a currency status, which makes most of its strength. As I developed in other articles, the US dollar waning role in the monetary system may be inevitable but it is unpredictable and could occur in a very distant future.

JPY re-appreciation could be also triggered by a coordinated – or not – action from major countries’ Central Banks in the forex market, including or not Japan. China and the US may be pushed for different reasons to compel or coordinated with Japan to re-appreciate its currency.

The end of the JPY carry trade in any scenario ?

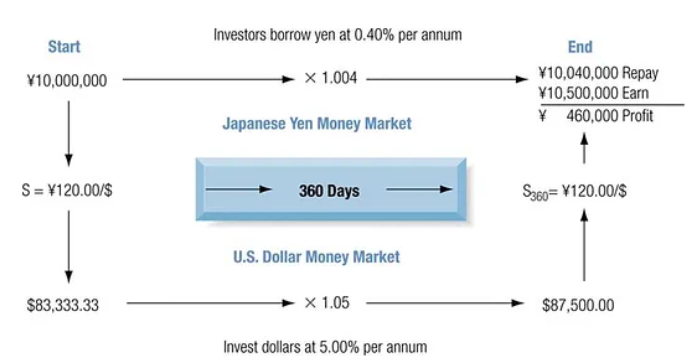

The Japanese carry trade refers to a widespread investment strategy among Anglo-saxon hedge funds notably, which consists in borrowing Yen and converting it into a currency with higher yields (the US dollar preponderantly) to buy then assets denominated in this currency. Under unchanged interest rates differential, the investor makes a riskless profit, as highlighted in the example below.

Japanese carry trade positions amounted to almost $1trn as of 2024 and go with derivatives positions that are much bigger. Indeed, the carry trade is a losing strategy if the Yen strengthens, which has pushed over the past few years traders with carry trade positions to hedge against a possible appreciation of the Yen by taking designated derivatives. This additional move jeopardizes the carry trade whatever the JPY evolution.

-if the US/JPY X-rate strengthens, traders may be faced with important losses even after selling their assets.

-if the US/JPY X-rate further weakens, the derivatives broker will require more collateral to the derivatives buyer (the carry trader). The hedging strategy is winning if the Yen suddenly appreciates, but actually is increasingly costly if the Yen durably weakens.

All in all, two things has to be remembered:

the increased general volatility of the Yen makes it a less desirable currency for carry trade, whatever its future evolution.

Cheap liquidity in Yen coupled with highly leveraged positions has been a major support for foreign stock markets and particularly the US stock market. The diminished access to Yen liquidity will press US stock prices downward. Disorderly closures of JPY carry trade positions may brutally impact the US stock market.

Conclusion

The short to medium-term context indicates the USD-JPY may further increase, especially in the absence of a rapid loosening of the US monetary policy, which is out of debate for now. However, in the long term, the US dollar future and Japan fundamentals will probably decrease the USD-JPY exchange rate. In the short-term, buying Japanese stocks of leading exporters in the automotive, machine tools and chemical industries and in the long -term buying Japanese Yen could be relevant. This scenario doesn’t take into account the Central Banks’ interventions in the forex market to control their currencies’ exchange rate with the Yen, but they are highly likely in the coming months.