Picture: a Deutsch Mark bill at the peak of Germany’s hyperinflation crisis, in 1923

note: i recommend to read my two articles about money for fully understanding the following article

“What most people and their countries want is wealth and power and money and credit are the biggest influencers on how wealth and power rise and decline. If you don’t understand how money and credit work, you can’t understand how the system works, and if you don’t understand how the system works, you can’t understand what is coming at you”.

These two sentences open Changing World Order chapter about the cycle of credit, money and growth. Ray Dalio underlines the importance of money and credit in a capitalist economy, yet he notes that neither the media, the educative system nor politicians explain what there are.

A few notions

We need to go back to basic principles, which Ray Dalio puts like this:

-Any individual, company or state could draw up its income statement, i.e. its expenses and revenues over the course of a calendar year. It could also write its balance sheet, which is different from an income statement, as it is an entity’s level of assets at a given moment. The balance sheet contains what is owed to others (liabilities or debts) and what is owned (assets).

-One person’s liabilities are another person’s assets and one person’s expenses are another person’s income. For example, a 100$ loan is a liability in the borrower’s balance sheet but an asset for the bank’s balance sheet.

-Debt has an expansive effect in the short term because it increases the debtor’s purchasing power, but it is recessionary in the long term because once the future repayment of the debt will absorb all real wealth. For example, someone who has borrowed to buy a house will at some point have to devote his revenues to payback its loan. But it may not be enough, i.e the interest expenses may end up being higher than the agent income. Therefore, he will have to sell his assets and use the cash from the selling of assets to pay off his debt. For example, many American households who had borrowed during the 2000’s to buy their house had to finally sell their house (asset) starting 2006 to have enough cash for paying back their mortgage loan, as their wages were insufficient.

On a broader scale, it explains the cyclical nature of the capitalist economy: phase A, credit boom, phase B, slowdown in activity linked to debt repayment.

The role of money- and credit-issuing institutions is therefore crucial in understanding both short-term and long-term cycles. Their classic role is in a credit economy is as follows

-In phase A, the economy risks deflation, i.e. a fall in prices because the supply of goods and services is lower than Demand. The commercial banks, with the support of the central bank, loosen credit conditions in order to revive the real economy. Agents have more money and credit, spend and invest more and their assets increase in value. Demand grows until it exceeds production capacity, generating inflation (the economy overheats) and until debt-related expenses grow faster than revenues. Then central banks start to tighten credit conditions by increasing rates.

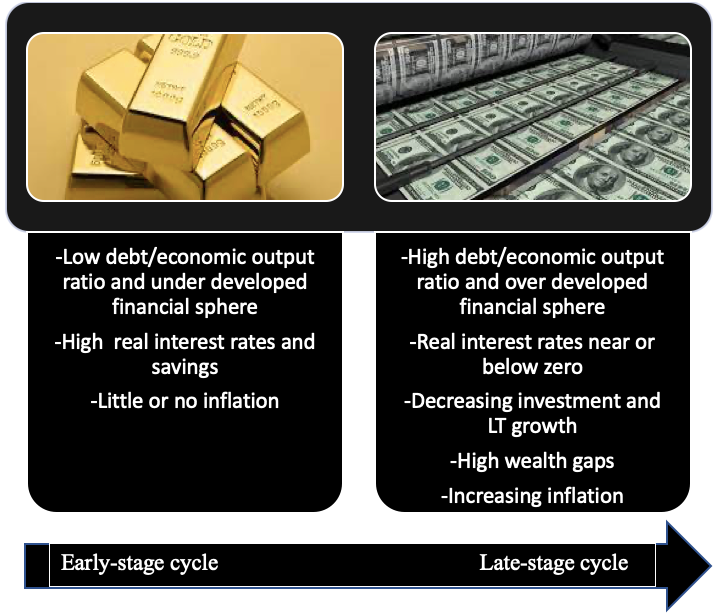

As seen in the article, money plays as a storehold of value, i.e. agents use money to save and not immediately spend all their income. But this ability to keep part of their income aside, and therefore their purchasing power, depends on the stability of the value of money. If money loses its value through inflation, people will be able to buy fewer things in 10 years’ time than they could today. This is why inflation kills any incentive to save money and ultimately, jeopardizes long-term growth, as savings are fueling most of an economy’s investment so production capacity.

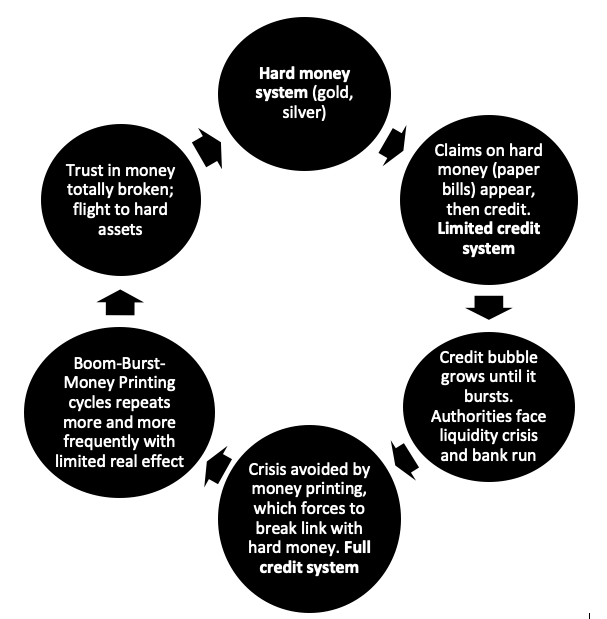

The Long-term Debt cycle is divided into 6 stages

Stage 1

At the beginning of the cycle, following a period of crisis and debt restructuring, the economy is purged of bad debts and the money used is so-called “hard” money, i.e. in the form of gold and silver coins. This as I have called it, the hard money system. Gold has an intrinsic value that is recognized by all and whose value does not depend on any human institution.

Stage 2

However, transporting gold and silver coins can be very inconvenient. That’s why very rapidly, hard currency is no longer used as such, but stored in banks and replaced by banknotes whose value was indexed to this stock. Historically, a banknote of value X is a right to claim a stock of gold of amount X from the bank. These notes we call today bills became the de facto currency because they were more practical, and were referred to as paper money. We enter the limited credit money system.

Stage 3

Credit always develops following adoption of paper bills. What is a debt? From the creditor’s point of view, it is the promise to receive money at a given time plus interest to reward the risk taken by the lender. More generally, the price of financial assets (bonds, shares, etc.) reflects the calculation of future income from these assets, so they are promises of income that depend on the performance of the real economy. For example, the price of a bond subscribed to by a company is a promise of income, the realization of which depends on the company’s economic performance, its ability to generate cash flow to pay its debts. The price of a share reflects expectations of the company’s future profits, and so on…

Credit growth turns into a bubble, i.e. the financial sphere (asset prices) becomes detached from the real sphere, i.e. promises of gains far exceed the capacity of companies to generate profits and produce, the capacity of households to increase their incomes, etc. This bubble is characterized by an increase in the debt (paper money)/hard money ratio.

Stage 4

The credit bubble bursts when debt holders realize that their promises of income (repayment + interest) will not be honored, because borrowers have too much debt. This is followed by a bank run and a liquidity crisis as everyone rushes to obtain cash, whether it is savers asking for their deposits or investors liquidating their entire portfolios. There is not enough liquidity to meet all these needs.

The central bank then has several choices: either it lets agents get rid of assets, particularly bonds, which would push up interest rates and bring borrowers to their knees, or it creates money to buy back bonds, thereby re-injecting money into the system. To do this, the Central Bank is obliged to make money no longer convertible into gold or silver, because the fixed convertibility regime effectively limits the quantity of paper money in circulation. The currency loses its anchorage to a reference, to a hard currency, and devalues

Stage 5

This brings us into monetary system 3, the full credit money system. Even if, of course, there are rules for issuing money, in theory the Central Bank can now create as much money as it wants. The devaluation and printing of money boosts the financial sector – property and financial assets rise – and avoids deflation by bailing out borrowers. This stimulates the economy and a new cycle is set in motion, but bubbles – the gap between the promises of the financial sphere and the capacities of the real economy – appear regularly. The Central Bank must therefore invariably make the same choices. To bring the debt/economic output ratio down to a reasonable level, it has four choices:

-Default on the debt: this means that politically influential groups of savers – the very rich, pensioners, foreign creditors – will receive nothing. Not acceptable.

–raise taxes to pay off public and private debt. Politically difficult to pass.

–austerity, reduce public spending, freeze wages so that private agents and the State can free up cash flow to pay down debt. Politically difficult to pass.

–PRINTING MONEY AND DEVALUING IT. This choice is the most acceptable for EVERYONE and even easier.

Governments use a bit of all four levers but mostly they end up repeating the same thing, printing money to buy back financial securities, bailing out etc, because that’s the easiest way, particularly now there is no longer the limit of the hard currency standard.

The same cycle of boom – burst – bail-out and money printing starts all over again, but the increase in the quantity of money has an increasingly minor effect on the real economy. Money remains in the financial sphere, which is increasingly uncorrelated from the real sphere. As the people holding assets represent only a tiny proportion of the population, inequalities are soaring and as we saw earlier, low saving rate (consequence of low interest rates to boost credit) mean low investment and future revenue growth prospects. However this period of prolonged money and credit growth can last a long time, particularly if this debt is issued in a reserve currency

Stage 6

This last stage stops when trust in the money is invariably broken. The psychological pattern is the same as previous bank-run phases, agents don’t trust anymore the banking system in its capacity to ensure a 100$ bill can actually buy goods worth 100$, or that a 100$ coupon will be paid back in due time. But this time, agents drop their paper money to get hard assets, i.e commodities and gold, or foreign currencies offering better interests rate or pegged to an hard asset. At this moment, the financial system of the country totally collapses and the authorities have to link the dying currency to a hard asset to restore trust. So the cycle restarts. This last stage last very quickly, as trust brutally reverses, max 3 years says Dalio.

As we will see in the last article, we are right now at the end of this Long-term Debt cycle which began in 1945 and which usually lasts 50-75 years. We are thus approaching the end of this cycle according to Dalio, and it also corresponds to the end of the Big Cycle of the American-ruled world order.

Appendix:

A) A summary of the Long-term Debt, Money and Economic activity cycle.

B) The general evolution of key indicators along the cycle

Leave a Reply